FinTech & Algorithmic Trading

Build high-performance trading systems with Rust, quantitative analysis, and ultra-low latency infrastructure

- What is Fintech Development?

- Fintech development is the creation of technology solutions for the financial services industry, combining finance and technology to build innovative products like payment systems, banking applications, trading platforms, and blockchain solutions. It requires specialized expertise in regulatory compliance (PCI-DSS, PSD2, GDPR), security best practices, real-time transaction processing, and integration with banking APIs and payment gateways. Fintech solutions must meet strict standards for data protection, audit trails, and financial regulations.

Dominate financial markets with high-performance algorithmic trading systems built in Rust for microsecond-level latency. I specialize in developing high-frequency trading (HFT) platforms, options market analysis systems, and quantitative trading strategies that execute thousands of trades per second with zero memory allocation in critical paths. My expertise spans market microstructure, order book analysis, and execution algorithms (TWAP, VWAP, Iceberg, Sniper) optimized for maximum alpha generation.

I design ultra-low latency trading infrastructure using kernel bypass technologies (DPDK, io_uring), FPGA acceleration for order routing, and direct market access (DMA) connections to major exchanges. My systems include real-time risk management, position monitoring, and automated circuit breakers that prevent catastrophic losses. I implement backtesting frameworks with historical market data, Monte Carlo simulations, and walk-forward optimization to validate strategies before live deployment.

Whether you need options pricing engines (Black-Scholes, Binomial, Monte Carlo), volatility surface modeling, or market-making strategies for crypto/forex/equities, I deliver production-ready solutions. From FIX protocol integration to cryptocurrency exchange APIs (Binance, Coinbase, Kraken), I build robust systems that handle market volatility, network failures, and exchange outages with zero data loss.

High-Frequency Trading (HFT)

- Rust trading engines with sub-microsecond latency

- Market microstructure analysis and order book modeling

- FPGA acceleration for order routing and matching

- Kernel bypass (DPDK, io_uring) for network optimization

Options Trading & Analysis

- Options pricing (Black-Scholes, Binomial, Monte Carlo)

- Implied volatility calculation and surface modeling

- Greeks calculation (Delta, Gamma, Vega, Theta, Rho)

- Volatility arbitrage and statistical arbitrage strategies

Quantitative Strategies

- Statistical arbitrage (pairs trading, mean reversion)

- Market making strategies with inventory management

- Machine learning models for price prediction and alpha generation

- Portfolio optimization and risk-adjusted returns (Sharpe, Sortino)

Risk Management & Compliance

- Real-time risk monitoring (VaR, CVaR, stress testing)

- Position limits and automated circuit breakers

- Trade surveillance and anomaly detection

- Regulatory compliance (MiFID II, Dodd-Frank, EMIR)

Backtesting & Simulation

- High-fidelity backtesting with historical tick data

- Monte Carlo simulations for strategy robustness testing

- Walk-forward optimization to prevent overfitting

- Paper trading environments for strategy validation

Exchange Connectivity

- FIX protocol integration for traditional exchanges

- Crypto exchange APIs (Binance, Coinbase, Kraken, FTX)

- WebSocket market data feeds with automatic reconnection

- Direct market access (DMA) with co-location support

FinTech & Trading Tools & Technologies

Trading Systems

Quant Libraries

Exchanges & Platforms

Data & Analytics

Business Impact of FinTech & Algorithmic Trading

Execute thousands of trades per second with microsecond-level latency

Generate consistent alpha through quantitative strategies and ML models

Manage risk in real-time with automated circuit breakers and position limits

Optimize options portfolios with precise Greeks calculation and hedging

Validate strategies with high-fidelity backtesting before live trading

Connect to multiple exchanges with FIX protocol and REST/WebSocket APIs

Why Work With Me

Direct access to 20+ years of hands-on expertise

20+ Years Experience

Two decades of real-world experience designing, building, and optimizing production systems for startups and enterprises alike.

AWS & GCP Certified

Certified cloud architect with deep expertise in AWS and Google Cloud Platform, ensuring best practices and optimal solutions.

Hands-On Technical Expert

I write code, configure infrastructure, and solve problems directly—no delegation to junior staff or outsourcing.

Proven Results

Track record of reducing infrastructure costs by 40-60%, improving performance, and delivering projects on time.

Direct Communication

Work directly with me—no account managers or intermediaries. Clear, technical discussions with fast response times.

Bilingual Support

Fluent in English and Spanish, serving clients across Europe, Americas, and worldwide with no communication barriers.

Frequently Asked Questions

Common questions about fintech development services

Fintech development is the creation of technology solutions for financial services, including payment processing systems, trading platforms, banking applications, and investment tools. It combines software engineering expertise with deep understanding of financial regulations, security requirements, and market dynamics. My fintech services cover algorithmic trading systems in Rust, payment gateway integrations, Open Banking implementations, and real-time transaction processing with sub-millisecond latency.

Digital transformation in finance is essential because traditional institutions face disruption from agile fintech startups and changing customer expectations. Modern consumers demand instant payments, mobile-first experiences, and 24/7 access to financial services. By implementing high-performance trading systems, automated compliance, and real-time analytics, financial organizations can reduce operational costs by 40-60%, improve customer satisfaction, and stay competitive in an increasingly digital marketplace.

Fintech development follows a rigorous process starting with regulatory compliance assessment and security architecture design. I then build proof-of-concept systems for validation, followed by iterative development with continuous testing against financial edge cases. Key phases include payment integration, security hardening, load testing for peak transaction volumes, and regulatory audits. The process typically takes 4-8 months for MVP, with ongoing iteration for feature expansion and compliance updates.

Fintech services benefit traditional banks modernizing legacy systems, startups building new financial products, investment firms requiring algorithmic trading platforms, payment companies scaling transaction processing, and enterprises needing secure financial integrations. Whether you are a hedge fund seeking low-latency trading infrastructure, a neobank building mobile payments, or an e-commerce platform integrating payment gateways, specialized fintech development ensures regulatory compliance and competitive performance.

Fintech development costs vary based on complexity, regulatory requirements, and security needs. A basic payment integration might start at $30,000-50,000, while comprehensive trading platforms range from $150,000-500,000+. Key cost factors include PCI-DSS certification requirements, multi-currency support, exchange integrations, and regulatory compliance across jurisdictions. I provide detailed estimates after analyzing your specific requirements, with transparent pricing that accounts for ongoing compliance and security maintenance.

For fintech applications, MVP typically takes 3-5 months, including basic payment processing or trading functionality with essential compliance features. Full production deployment requires an additional 2-4 months for security audits, penetration testing, regulatory certification, and stress testing under real-world transaction volumes. Algorithmic trading systems may require longer validation periods with paper trading before live deployment to ensure strategy robustness.

Fintech applications must comply with multiple regulations depending on their function and geography. PCI-DSS governs card payment security with 12 requirement domains. PSD2/PSD3 regulates European payment services with Strong Customer Authentication (SCA). MiFID II covers investment services and algorithmic trading. Additional requirements include GDPR for data protection, AML/KYC for anti-money laundering, and SOC 2 for operational security. I design systems with compliance built-in from the architecture level.

A fintech specialist brings deep domain expertise in financial regulations, payment protocols (FIX, SWIFT, SEPA), and security requirements that general developers lack. I understand market microstructure for trading systems, can implement proper audit trails for regulatory compliance, and know how to handle edge cases like split payments, chargebacks, and settlement failures. This specialized knowledge prevents costly compliance violations and security vulnerabilities that could result in regulatory fines or data breaches.

Fintech implementations deliver measurable outcomes including transaction processing at thousands of operations per second with sub-millisecond latency, 99.99% system uptime for mission-critical financial operations, and successful regulatory audits. Trading systems typically achieve execution speeds 10-100x faster than traditional platforms. Payment systems reduce transaction costs by 20-40% through optimized routing. User adoption rates improve by 30-50% with modern, mobile-first financial experiences.

I implement defense-in-depth security with end-to-end encryption (TLS 1.3, AES-256), HSM integration for key management, and zero-trust architecture. All systems include comprehensive audit trails for regulatory compliance, real-time fraud detection, and automated circuit breakers. Code is written in Rust for memory safety, eliminating common vulnerability classes. I provide security documentation for auditors, support during compliance certifications, and ongoing security maintenance with vulnerability scanning.

Getting started involves a discovery session to understand your business requirements, regulatory obligations, and technical constraints. I then conduct a compliance assessment to identify applicable regulations and security requirements. From there, I create a technical architecture proposal with cost estimates and timeline. Initial engagement typically includes a proof-of-concept to validate key integrations before full development begins, ensuring alignment with your business goals and risk tolerance.

My technical fintech capabilities include payment gateway integrations (Stripe, Adyen, PayPal), Open Banking APIs (Plaid, Tink, TrueLayer), cryptocurrency payment rails, and SWIFT/SEPA messaging. For trading, I build FIX protocol connectivity, WebSocket market data feeds, order management systems, and algorithmic execution engines. Infrastructure includes blockchain integration for DeFi applications, real-time analytics with TimescaleDB, and high-availability architectures with automatic failover.

Related Projects

Real-world implementations demonstrating this expertise

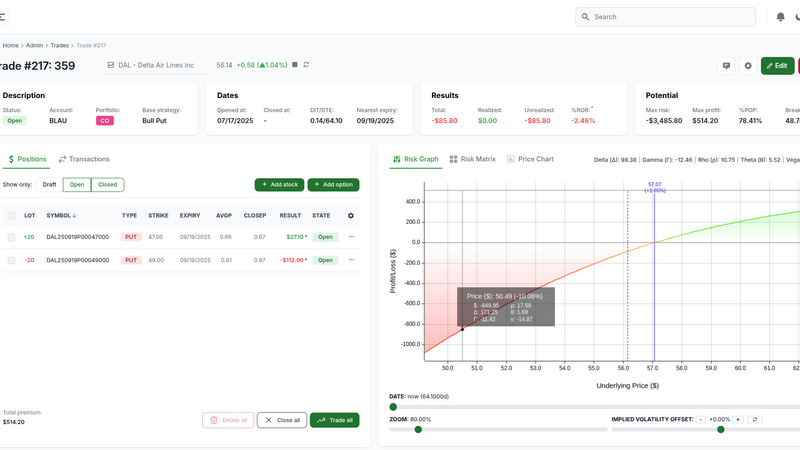

Option Panel - High-Performance Rust Options Trading Platform

Professional web-based options analysis platform combining the power of Rust and WebAssembly to perform complex financial calculations with exceptional performance, including Greeks analysis, multi-leg strategies, risk assessment and profitability evaluation with ultra-low latency.

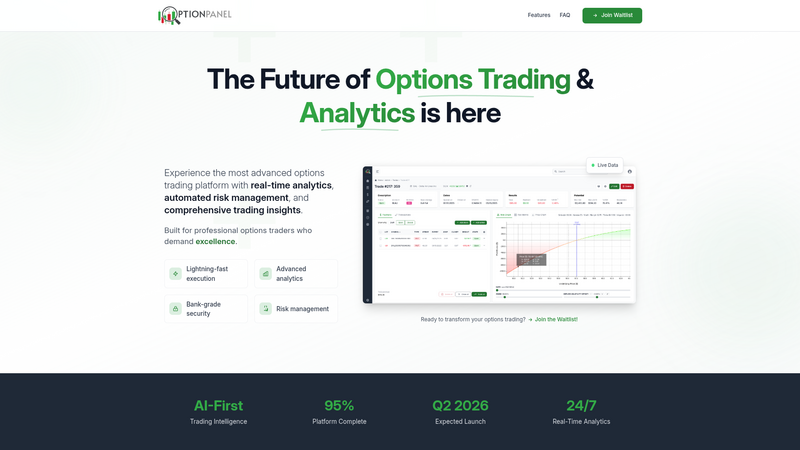

Option Panel - Modern Landing Page with Astro and Tailwind CSS

High-performance static landing page for professional options trading platform, built with Astro, Tailwind CSS, and JavaScript. Directus CMS integration for lead management with advanced spam and fraud protection. 1-week development timeline.

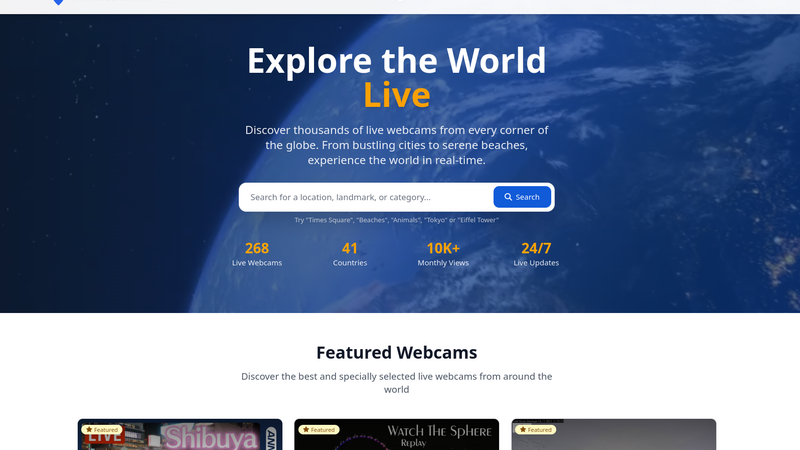

GeoWebcams - Intelligent Webcam Discovery Platform

Comprehensive platform combining Python data processing, Rust web applications, and AI-powered workflows to discover, validate, and serve thousands of live webcams from around the world, with advanced geographic search and live streaming capabilities.

Your expert

Daniel López Azaña

Cloud architect and AI specialist with over 20 years of experience designing scalable infrastructures and integrating cutting-edge AI solutions for enterprises worldwide.

Learn more